© Real Estate Finance Forum All rights reserved.

Use of these names, logos, and brands does not imply endorsement unless specified. By using this site, you agree to the Privacy Policy and Terms & Conditions.

Rendering of the Bioforge Marshall plant, which is currently under construction. Image courtesy of Solugen Climate technology company Solugen has...

A rendering of the completed Rockefeller Group Logistics Center at Roosevelt Boulevard, which will lie within a day’s drive of...

DataBank has established a new $725 million credit facility which it intends to use to finance ongoing and future data...

A Queens condominium with a coveted 421a state tax abatement didn’t hold up its end of the deal, Comptroller Brad...

Hudson’s Site rises 681 feet in downtown Detroit. Image courtesy of Bedrock Bedrock has topped out The Tower of the...

Jun Ho Pok of IGIS Neovalue Asset Management, Kevin Davenport of Swire Properties and Megumi Brod of The Rockefeller Group...

The Austin office market started the year off with solid investments, in what was a change of pace from 2023’s...

Inflation rose higher this past month than at any point since September 2023, and housing and gas prices were largely...

Rendering of Factory Shoals Distribution Center, that will come online in late 2024. Image courtesy of CommercialEdge Cushman & Wakefield...

As the year kicked off, Houston’s office market still struggled with low activity and occupancy, according to CommercialEdge data. The...

Rendering of the Bioforge Marshall plant, which is currently under construction. Image courtesy of Solugen Climate technology company Solugen has...

A rendering of the completed Rockefeller Group Logistics Center at Roosevelt Boulevard, which will lie within a day’s drive of...

DataBank has established a new $725 million credit facility which it intends to use to finance ongoing and future data...

A Queens condominium with a coveted 421a state tax abatement didn’t hold up its end of the deal, Comptroller Brad...

Hudson’s Site rises 681 feet in downtown Detroit. Image courtesy of Bedrock Bedrock has topped out The Tower of the...

Jun Ho Pok of IGIS Neovalue Asset Management, Kevin Davenport of Swire Properties and Megumi Brod of The Rockefeller Group...

The Austin office market started the year off with solid investments, in what was a change of pace from 2023’s...

Inflation rose higher this past month than at any point since September 2023, and housing and gas prices were largely...

Rendering of Factory Shoals Distribution Center, that will come online in late 2024. Image courtesy of CommercialEdge Cushman & Wakefield...

As the year kicked off, Houston’s office market still struggled with low activity and occupancy, according to CommercialEdge data. The...

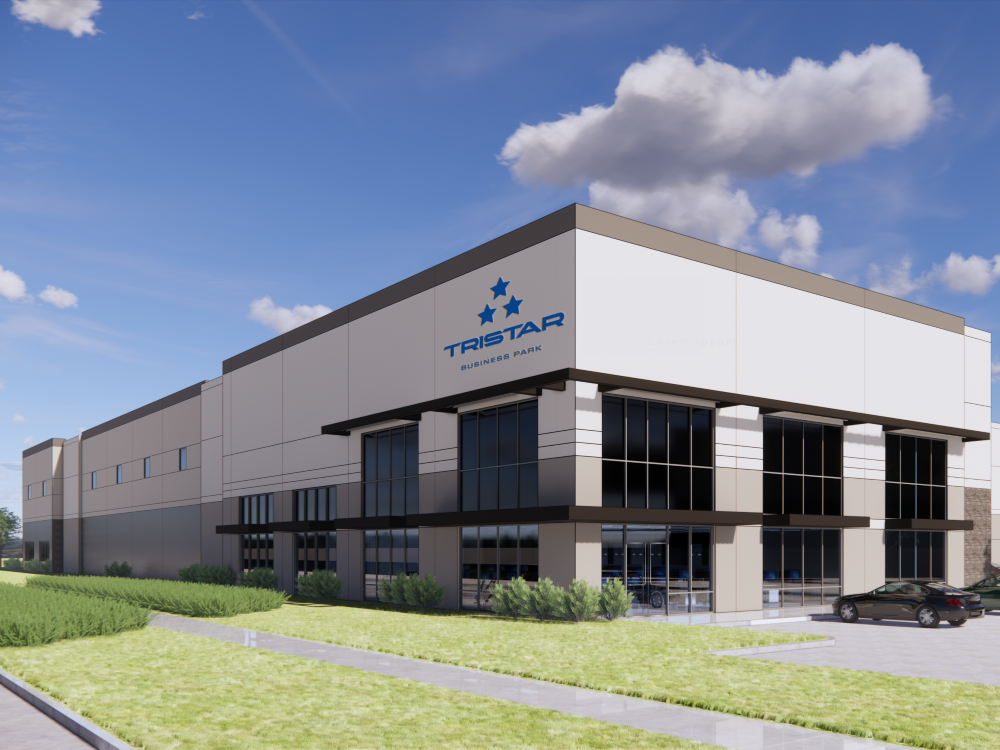

The 10-acre Tristar Business Park will feature two industrial building totaling 173,680 square feet. Image courtesy of Colliers A joint...

CMBS office debt was paid off at an increased rate to start the year, but a deeper look at the...

")

© Real Estate Finance Forum All rights reserved.

Use of these names, logos, and brands does not imply endorsement unless specified. By using this site, you agree to the Privacy Policy and Terms & Conditions.